The call came in at 11 p.m. from Dingboche, 4,410 metres above sea level, two days below Everest Base Camp.

One of our clients, a fit 42-year-old from London, had developed a severe headache, lost coordination, and could no longer walk a straight line. These were the textbook signs of High Altitude Cerebral Edema (HACE). He needed an emergency helicopter evacuation to Kathmandu within hours, not tomorrow morning.

The helicopter was arranged. He survived and recovered fully. The total cost of that rescue? $4,800 USD.

His travel insurance policy? It covered trekking up to 4,000 metres. Dingboche sits at 4,410 metres. He was 410 metres too high, and faced every dollar of that bill himself.

This is the single most common, most costly, and most preventable insurance mistake we see at Mount Everest Go. And we see it every season.

What Your Nepal Trekking Insurance Must Cover (The Quick Answer)

| The Essential Checklist — Read This First |

| Your Nepal trekking insurance must include ALL of the following: |

| ✔ High-altitude coverage to at least 6,000m (or 8,848m for Everest Base Camp treks) |

| ✔ Emergency helicopter evacuation — no sub-limits, no co-pay exclusions |

| ✔ Search and rescue operations (separate from medical evacuation) |

| ✔ Acute Mountain Sickness (AMS), HACE, and HAPE treatment |

| ✔ Medical repatriation to your home country |

| ✔ Trip cancellation and curtailment |

| ✔ 24/7 emergency assistance hotline with Nepal-specific experience |

| ❌ Most standard travel insurance policies cover NONE of the above adequately. |

| Policies marketed as ‘adventure travel’ often cap helicopter evacuation at $10,000 USD, a Himalayan rescue can cost $3,000–$8,000 for the flight alone, plus hospital costs. |

Understanding Altitude Illness: AMS vs HACE vs HAPE

Before we talk about insurance, you need to understand what you’re insuring against. Altitude illness comes in three forms, each more serious than the last. Your insurance must explicitly cover all three.

| Condition | AMS (Acute Mountain Sickness) | HACE (Cerebral Edema) | HAPE (Pulmonary Edema) |

| Onset Altitude | 2,500m+ (e.g., Namche Bazaar at 3,440m) | 3,500m+ (e.g., Tengboche, 3,867m) | 3,000m+ (can develop rapidly) |

| Key Symptoms | Headache, nausea, fatigue, dizziness, poor sleep | Severe headache, loss of coordination, confusion, unconsciousness | Breathlessness at rest, pink frothy sputum, rapid heart rate, extreme fatigue |

| Emergency Level | Moderate — rest and acclimatise | CRITICAL — immediate descent and evacuation | CRITICAL — immediate descent, oxygen, evacuation |

| Typical Evacuation Cost | Usually none if caught early | $4,000–$8,000 helicopter + hospital | $5,000–$10,000+ helicopter + ICU care |

| Covered by Standard Travel Insurance? | Often yes, if below 4,000m altitude cap | Rarely — altitude caps and exclusions apply | Rarely — altitude caps and exclusions apply |

The Altitude Cap Problem: Why 4,000m Is Not Enough

I’ve guided treks in Nepal for over 14 years. When I check a client’s insurance before they leave Kathmandu, I see the same dangerous pattern repeatedly: policies capped at 4,000 metres, sometimes 5,000 metres. Let me show you why that’s not good enough on most popular treks.

| Trek / Key Campsite | Altitude | Covered by 4,000m Policy? | Covered by 6,000m Policy? |

| Namche Bazaar (EBC Trek) | 3,440m | ✔ Yes | ✔ Yes |

| Tengboche Monastery | 3,867m | ✔ Yes (barely) | ✔ Yes |

| Dingboche (EBC Trek) | 4,410m | ❌ No — 410m over limit | ✔ Yes |

| Lobuche (EBC Trek) | 4,940m | ❌ No | ✔ Yes |

| Everest Base Camp | 5,364m | ❌ No | ✔ Yes |

| Kala Patthar (EBC Trek) | 5,643m | ❌ No | ✔ Yes |

| Thorong La Pass (Annapurna Circuit) | 5,416m | ❌ No | ✔ Yes |

| Mera Peak Summit | 6,476m | ❌ No | ✔ Yes (just) |

| Island Peak Summit | 6,189m | ❌ No | ✔ Yes |

Bottom line: If you’re trekking anywhere above Namche Bazaar on the Everest route, or above Manang (3,519m) on the Annapurna Circuit, a 4,000m altitude cap leaves you dangerously exposed.

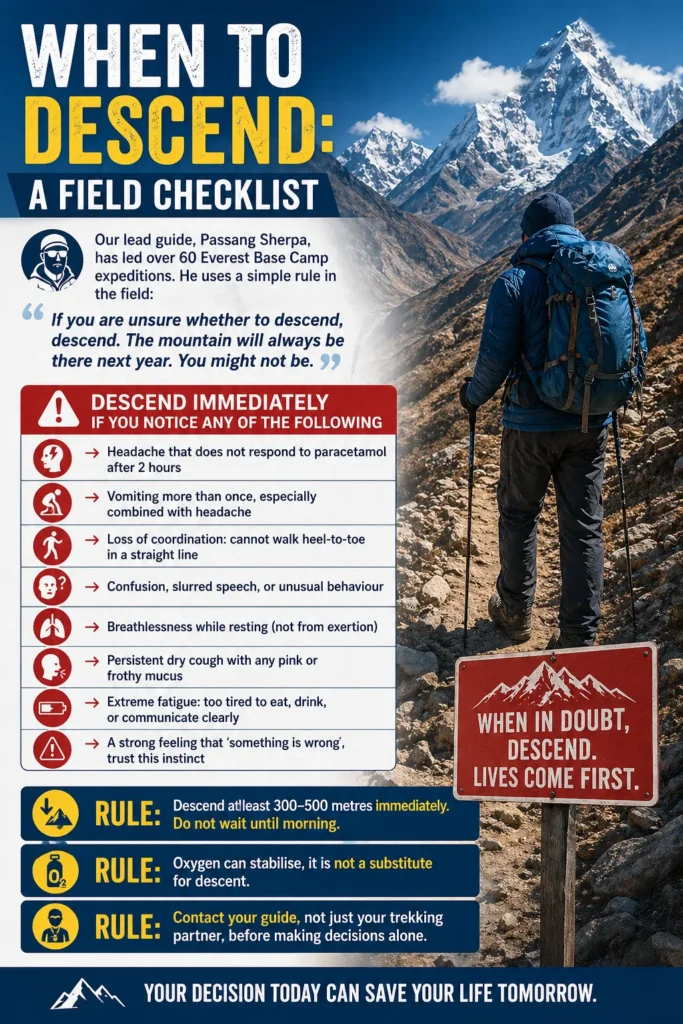

When to Descend: A Field Checklist

Our lead guide, Passang Sherpa, has led over 60 Everest Base Camp expeditions. He uses a simple rule in the field:

“If you are unsure whether to descend, descend. The mountain will always be there next year. You might not be.”

| 🚨 Descend Immediately If You Notice ANY of the Following |

| → Headache that does not respond to paracetamol after 2 hours |

| → Vomiting more than once, especially combined with headache |

| → Loss of coordination: cannot walk heel-to-toe in a straight line |

| → Confusion, slurred speech, or unusual behaviour |

| → Breathlessness while resting (not from exertion) |

| → Persistent dry cough with any pink or frothy mucus |

| → Extreme fatigue: too tired to eat, drink, or communicate clearly |

| → A strong feeling that ‘something is wrong’, trust this instinct |

| RULE: Descend at least 300-500 metres immediately. Do not wait until morning. |

| RULE: Oxygen can stabilise, it is not a substitute for descent. |

| RULE: Contact your guide, not just your trekking partner, before making decisions alone. |

Insurance Options Compared: What Trekkers Actually Buy

Here is an honest comparison of the insurance categories we see clients arrive with, and what they actually cover:

| Insurance Type | Altitude Cap | Heli Evacuation | Approx Cost | AMS/HACE/HAPE Covered? | Our Verdict |

| Standard Travel Insurance | None listed — but medical exclusions apply | Often excluded or capped at $10,000 | $50–$150 | Rarely explicitly covered | ❌ Not sufficient |

| Adventure Travel (Budget) | Typically 4,000m–5,000m | $50,000–$100,000 limit | $80–$200 | Sometimes, if under altitude cap | ⚠ Risky for EBC |

| Specialist Trek Insurance (Mid) | 6,000m standard | $200,000–$500,000 unlimited | $150–$350 | Yes, explicitly | ✔ Good for most treks |

| Himalayan/High Altitude Specific | Up to 8,848m | Unlimited or $500,000+ | $250–$600 | Yes, fully explicit | ✔✔ Best — required for peaks |

| Annual Multi-Trip (Adventure Add-on) | Varies — read carefully | Varies widely | $400–$900/year | Depends on policy add-ons | ⚠ Verify altitude cap |

Recommended providers with proven Himalayan track records (verify current terms before purchasing): World Nomads, True Traveller, Battleface, Dogtag, and Global Rescue. Always call and confirm altitude coverage verbally, then get it in writing.

Step into the heart of the Himalayas and follow the legendary trail to Everest Base Camp. This 14-day adventure blends…

The Sherpani Col Pass Trek is a 24–30 day high-altitude expedition linking Makalu Barun National Park to the Everest region….

The Serang Gompa Trek is a profound journey into the "Hidden Valley of Kyimolung," one of the sacred Beyuls (hidden…

A challenging and rewarding 16-day adventure combining Gokyo Cho La Pass, and Everest Base Camp. The Gokyo Chola Pass Everest…

Shey Phoksundo Lake trek on a 12-day guided adventure. Explore the remote Dolpo region, witness the unique Bon culture, and…

The Saipal Himal Base Camp Trek is a 20-day adventure into one of Nepal’s most remote and unexplored regions. This…

The Nar phu Valley and Tilicho Mesokanto Pass Trek is an off-the-beaten-path Himalayan journey that takes you through the hidden…

The Top 5 Objections We Hear, And The Honest Answers

“I’m young and fit. I don’t need extra insurance.”

Altitude illness does not care how fit you are. It is not a fitness problem, it is a physiological response to reduced oxygen at elevation. We have evacuated marathon runners, military veterans, and professional athletes from the trail between Dingboche and Lobuche. Fitness is an advantage in many ways, but it provides zero protection against HACE or HAPE. Some research even suggests that highly motivated, fit trekkers push through early AMS symptoms because they are accustomed to discomfort, which can accelerate deterioration.

“The insurance is too expensive.”

A proper high-altitude policy for a 3-week Nepal trek typically costs $200–$400 USD. A helicopter evacuation from above 5,000m costs $4,000–$8,000. Hospitalisation in Kathmandu for altitude-related complications adds another $2,000–$15,000. The maths is straightforward. The insurance is not expensive. The consequences of not having it are.

“My credit card travel insurance covers me.”

Read your credit card policy carefully, specifically the section on altitude limits, adventure activity exclusions, and helicopter evacuation sub-limits. In our experience, fewer than 10% of credit card travel insurance policies adequately cover trekking above 4,000m. Most have a $10,000–$25,000 evacuation cap. A single high-altitude rescue, hospitalisation, and medical repatriation to Europe or North America can exceed $50,000 USD. Print the policy, highlight the altitude clause, and show it to your guide.

“I’ll just be careful and not get sick.”

Nobody plans to get altitude illness. Nobody chooses it. The physiology is partly genetic, you will not know how your body responds to extreme altitude until you are there. We have had experienced trekkers who completed Everest Base Camp four times without incident develop serious HACE on their fifth trip. The altitude is unpredictable. The insurance is predictable. Get the insurance.

“Can’t I just buy insurance in Kathmandu?”

You can purchase insurance in Thamel, Kathmandu, and some local policies are legitimate. However, we strongly advise purchasing before you leave your home country for three reasons: (1) Pre-existing conditions are far more likely to be excluded if you buy last-minute. (2) Policy documentation and claims processing is smoother with a provider in your home jurisdiction. (3) You can research, compare, and call the insurer from home, not from a teahouse in Namche the night before you ascend.

Exactly What to Tell Your Insurance Provider

When you call or chat with an insurer, ask these exact questions. Write down the agent’s name and the time of the call.

- “Does this policy cover trekking or mountaineering above 6,000 metres in the Himalayas of Nepal?”

- “Does it cover emergency helicopter evacuation from altitude — with no sub-limit or co-payment?”

- “Are Acute Mountain Sickness, HACE, and HAPE explicitly listed as covered conditions?”

- “Does it cover search and rescue operations, separate from medical evacuation?”

- “Is there a 24/7 emergency line that has experience arranging Nepal helicopter rescues?”

- “What is the total maximum payout for medical and evacuation costs combined?”

If the agent cannot answer these questions clearly and confidently, that is your answer. Find a different insurer.

A Note From the Trail: What Your Guide Will Ask About Your Insurance

At Mount Everest Go, our guides are trained to ask every client about their insurance before the trek begins, ideally in Kathmandu, during the briefing, not on the trail above Namche.

We ask clients to show us the policy page that lists: altitude coverage, evacuation limit, and emergency contact number. We store the emergency number in our own satellite phone. This has saved lives.

In the Khumbu region, our relationships with Simrik Air, Fishtail Air, and other helicopter operators mean we can arrange evacuation rapidly, but only if the insurance company is cooperative. Policies from unknown providers with no Nepal experience cause delays. Delays at altitude can be fatal.

If your policy does not have a 24/7 emergency line, a real one, with a human on the other end who knows what Tengboche or Lobuche means, it is not adequate for Himalayan trekking.

| 📋 Quick Reference: Permits Required for Major Nepal Treks |

| Sagarmatha National Park (EBC Trek): NRS 3,000 (~$22 USD) — Monjo checkpoint |

| TIMS Card (all major treks): NRS 2,000 (~$15 USD) — Nepal Tourism Board, Kathmandu |

| Annapurna Conservation Area Permit: NRS 3,000 (~$22 USD) — ACAP offices |

| Manaslu Circuit (Restricted Area): USD $70–$100/week — must use registered guide |

| Upper Mustang (Restricted Area): USD $500 for 10 days — must use registered guide |

| Important: Your insurance may require proof of registered guide and valid permits for any rescue claim to be valid. Trekking without permits in restricted areas can void your policy entirely. |

Before You Book: Talk to Someone Who Has Done This 100 Times

We have been guiding trekkers in Nepal since 2009. Our guides have accompanied clients through AMS in Namche, HAPE scares in Dingboche, and successful, beautiful, life-changing summits of Everest Base Camp, Kala Patthar, and the Annapurna Circuit.

We do not sell insurance. But we will sit down with you before your trek, in Kathmandu, and help you read your policy, identify gaps, and make sure you’re properly covered. That is part of what you get when you trek with a local company that genuinely cares about bringing you home safely.

Frequently Asked Questions

1. Does World Nomads cover helicopter evacuation in Nepal above 5,000m?

World Nomads Explorer plan covers trekking to high altitudes including Everest Base Camp, and includes emergency evacuation. However, you must select the correct activity (“trekking” or “mountaineering” as appropriate) when purchasing, and the altitude limit depends on your plan tier. Always verify your specific policy’s altitude cap and evacuation limit before purchasing. Call World Nomads directly and ask about coverage above 5,000m in Nepal, their agents are generally knowledgeable about Himalayan treks.

2. Can I get trekking insurance with a pre-existing medical condition for Nepal?

Yes, but it is more complex. Several specialist insurers, including True Traveller and Battleface, offer policies that can cover pre-existing conditions, sometimes with an additional premium or after a medical screening. Disclose all conditions fully: non-disclosure is the number one reason altitude-illness claims are rejected. Conditions like controlled hypertension, asthma, or previous cardiac events require specialist insurer assessment. Do not trek without confirmed coverage for your specific conditions.

3. What happens if I don’t have insurance and need a helicopter evacuation in Nepal?

You will be required to pay cash upfront, or provide a confirmed credit card guarantee, before the helicopter departs. In some cases, your trekking company or the Himalayan Rescue Association can provide emergency assistance, but this is not guaranteed. If you cannot pay, evacuation may be delayed. In altitude emergencies, delay is life-threatening. The Nepalese government does not provide free emergency evacuation services. Some embassies can assist with repatriation in extreme cases, but not with in-country rescue costs.

4. Is trekking insurance different from climbing insurance in Nepal?

Yes, significantly. Trekking insurance covers non-technical trails, including Everest Base Camp, Annapurna Circuit, Langtang, and similar routes. Climbing or mountaineering insurance covers technical ascents using ropes, crampons, and ice axes, including peaks like Island Peak (6,189m), Mera Peak (6,476m), or Lobuche East (6,145m). If your trek includes any summit attempt on a technical peak, you must have mountaineering insurance, not just trekking insurance. Your permit category will determine which applies.

5. How do I file an insurance claim for altitude illness or helicopter evacuation in Nepal?

Call your insurer’s emergency line immediately, do not wait until after the evacuation. Your guide should also have this number. Document everything: save all hospital receipts, the helicopter operator’s invoice (companies like Simrik Air or Fishtail Air provide official documentation), all medical reports, and a written account of symptoms and timeline. In Nepal, the Himalayan Rescue Association clinics at Pheriche (4,371m) and Manang (3,519m) can provide medical certificates documenting altitude illness diagnosis. Submit your claim within the window specified in your policy, usually 30 to 90 days after the incident.

| ⚕ Medical Disclaimer |

| This article provides general trekking guidance only. Always consult a qualified medical professional before undertaking high-altitude trekking. Individual health conditions vary significantly. This is not medical advice. |